Cache Log Tr (K2LU.SI) has fallen 9.3% from Jan 2018 high. Looks attractive with yield of 8.37%. But I am holding back from any purchase. I currently do no hold shares of Cache Log Tr.

Here are some of my thoughts:

1) NAV per unit has not grown

Latest slides show portfolio valuation has increased with increased number of properties:

However, factoring additional units issued, the NAV per unit has plateaued in the last 5 years:

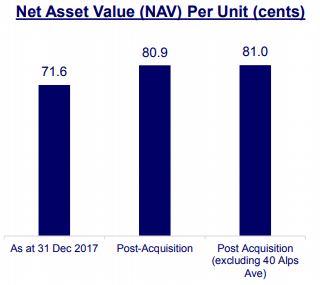

Before the acquisition of 9 properties in Australia, this was presented as one of the justification of purchase:

Note the NAV of 0.716 as at 31 Dec 2017, and the projected 0.81 post acquisition.

Now, after the purchase of 9 properties, and sale of 40 Alps:

At S$0.705, the NAV per unit is even lower than corporate actions that began last year!

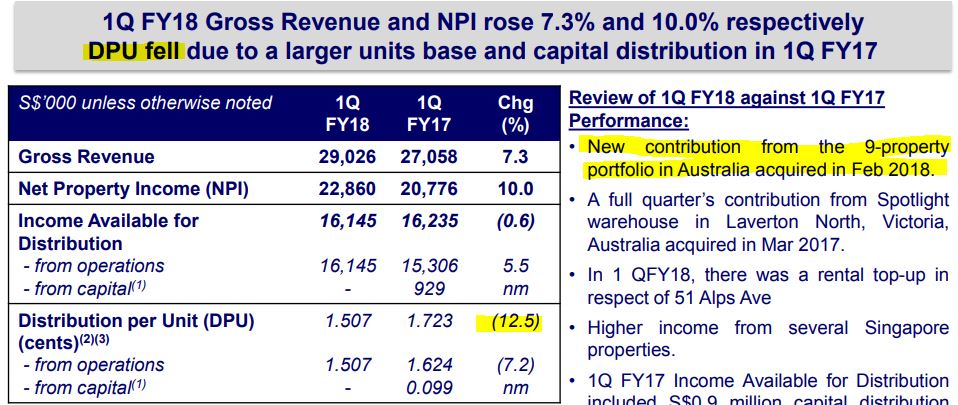

2) DPU decreased even after factoring 9 properties acquired in Feb 2018.

Revenue increased. NPI increased. But DPU fell. It also fell year on year (not shown).

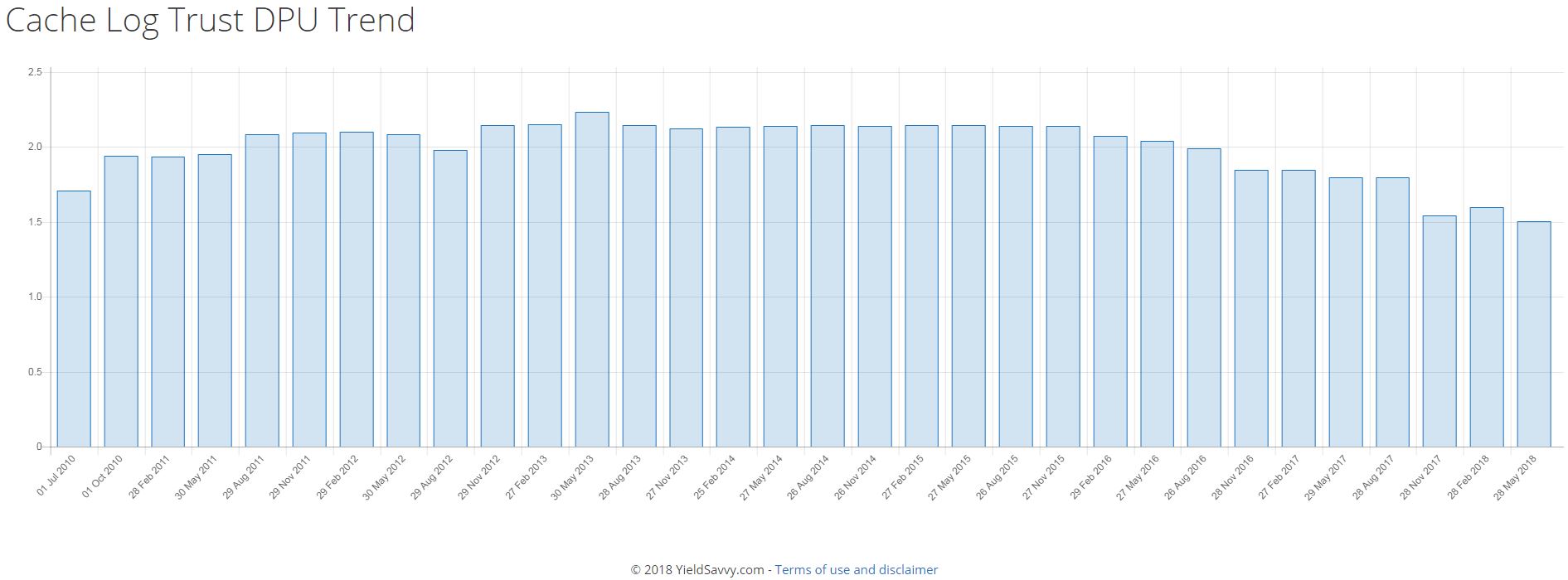

3) DPU trend continues to fall after corporate actions:

Why Cache went through with these corporate actions, when both NAV and DPU continues to fall.

The total transaction cost including Manager’s acquisition fee, professional fees and other transaction fees and expenses was S$3.8M.

- I'm a remisier with Maybank Securities, and as a bonds and REITs investor myself, I guide my clients to build resilient bonds and REITs portfolios. If you like to be guided, please open a trading account to become my client; It's free!

- WealthLions is my blog where I journal my trading ideas and share my opinions about the markets. If you like to be kept posted of my new blog posts and events, please join my Telegram Channel and subscribe to my mailing list. No spam, I promise.