Since 20 July 2017 when Hyflux posed a negative profit guidance:

- Hyflux shares has fallen 8.11%, from 0.555 to 0.510

- Hyflux 6% CPS 2018 has fallen 2.89% from 100.50 to 97.55

- Hyflux 6% PCS 2020 has fallen 6.16% from 0.99 to 0.929

Some facts:

- Besides water processing, Hyflux is also into electricity generation and waste management.

- Hyflux posted net loss for 2nd Q 2017 results citing “weak Singapore power market“.

- Hyflux is now late in their payment of dividends to their shareholders. A check with SGX’s Corporate Action page reveals that since 2011, Hyflux recorded date for their 2H dividend payment has never been later than Aug.

- When Hyflux perp prices “plunged” last week, Hyflux share prices went up slightly. How to make head or tail of this?

- Hyflux looking to sell their Tianjin Dagang desalination plants and the Tuaspring Integrated Water and Power Project.

- Hyflux have serious short term liquidity and short term working capital issues. They will need to rely on asset sales to meet their short term obligations.

My view:

- I already assuming that Hyflux 2018 perps will not be paying their Oct 2017 and Apr coupons – till their asset sales have completed. Fortunately for perp holders, unpaid coupons will be cumulative.

- I am also assuming that they will not be calling back the perps on Apr 2018 perps. The coupon will reset to 8%. Hyflux 2018 perps may be redeemed on 25 Apr 2018 and any date after. Once the asset sales are completed, they will likely want to call back the perp as they would not want to pay the 8% coupons for long.

- I will not compare Hyflux with Swiber or Noble. The former has close to zero sales, while the latter is primarily a trading company. Hyflux has an order book of almost S$3B as of June 2017, and they own assets of value, some of national value.

- They are building the S$750M TuasOne Waste to Energy project due to complete in 2019. It will have hard to imagine Hyflux going kaput before they can complete.

- I do buy the Hyflux story of increasing water demand, sustainable waste management, land efficient and energy efficient solutions – if they overcome their short term issues.

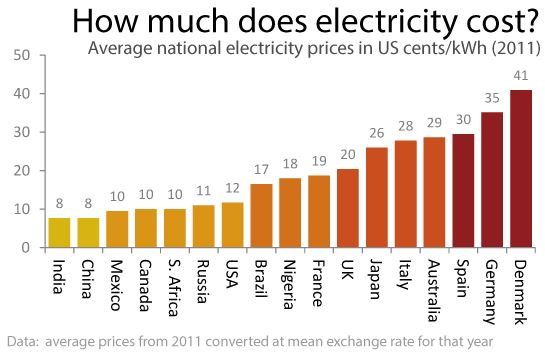

- Hyflux blamed their poor results on low cost of electricity in Singapore. It may also be due to consumption was lower than projected. I initially did not understand it as I know from my general knowledge that Russia’s electricity is 10x cheaper than Singapore’s. How can Singapore’s electricity continue to increase when it is already so expensive? Well Google shed some light:

I am paying about US$0.15 per kWH for my electricity bills, which puts Singapore somewhere in the middle of this 2011 chart. It is altogether plausible that as our electricity bills increases to that of Western nations, Hyflux will stand to benefit.

- I'm a remisier with Maybank Securities, and as a bonds and REITs investor myself, I guide my clients to build resilient bonds and REITs portfolios. If you like to be guided, please open a trading account to become my client; It's free!

- WealthLions is my blog where I journal my trading ideas and share my opinions about the markets. If you like to be kept posted of my new blog posts and events, please join my Telegram Channel and subscribe to my mailing list. No spam, I promise.